All Categories

Featured

Table of Contents

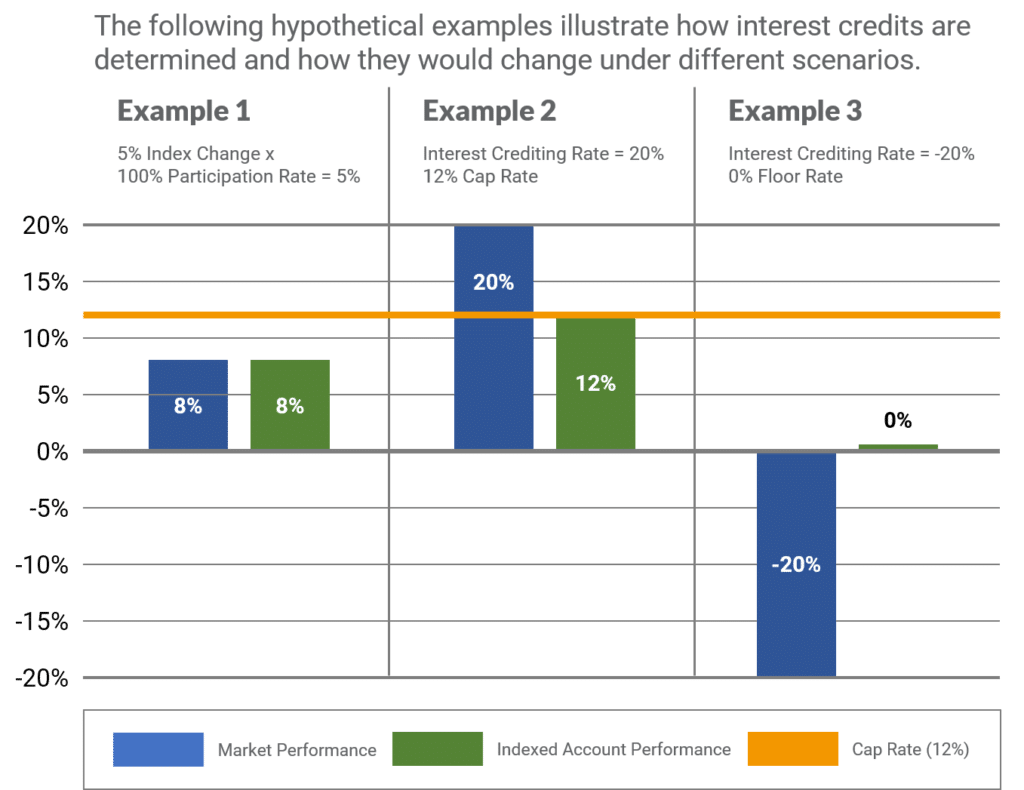

For gaining a limited quantity of the index's development, the IUL will never ever obtain less than 0 percent passion. Also if the S&P 500 decreases 20 percent from one year to the next, your IUL will not lose any kind of money value as an outcome of the market's losses.

Talk concerning having your cake and eating it as well! Imagine the passion intensifying on a product keeping that sort of power. Offered all of this information, isn't it conceivable that indexed global life is an item that would certainly allow Americans to acquire term and invest the rest? It would certainly be hard to refute the reasoning, wouldn't it? Now, do not obtain me incorrect.

A true investment is a protections item that is subject to market losses. You are never ever based on market losses with IUL just since you are never ever subject to market gains either. With IUL, you are not purchased the market, yet simply gaining interest based upon the performance of the market.

Returns can expand as long as you proceed to make settlements or keep a balance. Contrast life insurance policy online in mins with Everyday Life Insurance Coverage. There are two sorts of life insurance coverage: permanent life and term life. Term life insurance just lasts for a certain duration, while irreversible life insurance policy never ends and has a money worth component along with the survivor benefit.

Indexed Whole Life Insurance

Unlike global life insurance policy, indexed global life insurance policy's money worth makes rate of interest based upon the efficiency of indexed securities market and bonds, such as S&P and Nasdaq. Bear in mind that it isn't straight bought the securities market. Mark Williams, CEO of Brokers International, discusses an indexed global life plan resembles an indexed annuity that seems like universal life.

Universal life insurance coverage was produced in the 1980s when passion prices were high. Like various other types of permanent life insurance policy, this policy has a cash money worth.

Indexed global life policies offer a minimal surefire passion price, additionally known as an interest crediting floor, which decreases market losses. State your cash value sheds 8%.

Universal Life Cash Value Calculator

It's also best for those prepared to assume extra threat for greater returns. A IUL is a long-term life insurance policy policy that obtains from the buildings of a global life insurance policy policy. Like universal life, it enables versatility in your survivor benefit and premium repayments. Unlike universal life, your cash value expands based upon the performance of market indexes such as the S&P 500 or Nasdaq.

Her work has actually been published in AARP, CNN Highlighted, Forbes, Fortune, PolicyGenius, and U.S. Information & World Report. ExperienceAlani has reviewed life insurance policy and pet dog insurance provider and has actually composed many explainers on traveling insurance policy, debt, financial obligation, and home insurance coverage. She is enthusiastic regarding demystifying the complexities of insurance coverage and various other individual money subjects to ensure that viewers have the info they need to make the best cash decisions.

Paying only the Age 90 No-Lapse Premiums will certainly assure the fatality benefit to the insured's obtained age 90 however will certainly not assure cash money worth accumulation. If your customer terminates paying the no-lapse warranty premiums, the no-lapse function will end prior to the ensured duration. If this takes place, added premiums in an amount equal to the shortage can be paid to bring the no-lapse function back effective.

I recently had a life insurance policy salesman appear in the remarks thread of a message I published years ago concerning not blending insurance and investing. He believed Indexed Universal Life Insurance Policy (IUL) was the very best thing given that cut bread. In assistance of his position, he published a link to an article written in 2012 by Insurance Coverage Representative Allen Koreis in 2012, qualified "16 Reasons that Accountants Prefer Indexed Universal Life Insurance Policy" [link no more available]

Cost Insurance Life Universal

Initially a quick description of Indexed Universal Life Insurance Coverage. The attraction of IUL is noticeable.

If the marketplace decreases, you obtain the ensured return, usually something between 0 and 3%. Obviously, considering that it's an insurance coverage, there are also the common expenses of insurance, compensations, and surrender costs to pay. The details, and the reasons that returns are so horrible when blending insurance policy and investing in this specific method, boil down to essentially three things: They just pay you for the return of the index, and not the returns.

Max Funded Life Insurance

Your optimum return is covered. So if you cap is 10%, and the return of the S&P 500 index fund is 30% (like in 2015), you get 10%, not 30%. Some plans just give a particular percent of the modification in the index, say 80%. So if the Index Fund goes up 12%, and 2% of that is dividends, the modification in the index is 10%.

Include all these effects together, and you'll locate that lasting returns on index universal life are rather darn close to those for whole life insurance coverage, positive, but low. Yes, these plans assure that the money worth (not the cash that mosts likely to the costs of insurance, of course) will certainly not lose money, yet there is no warranty it will certainly maintain up with rising cost of living, a lot less grow at the rate you require it to grow at in order to attend to your retirement.

Koreis's 16 factors: An indexed global life policy account worth can never shed cash because of a down market. Indexed universal life insurance policy warranties your account value, locking in gains from each year, called a yearly reset. That's real, however only in nominal returns. Ask yourself what you require to pay in order to have a warranty of no small losses.

In investing, you make money to take threat. If you do not want to take much risk, do not anticipate high returns. IUL account worths expand tax-deferred like a certified strategy (individual retirement account and 401(k)); mutual funds do not unless they are held within a qualified plan. Basically, this means that your account value advantages from three-way compounding: You earn interest on your principal, you make interest on your interest and you earn rate of interest accurate you would or else have actually paid in taxes on the passion.

Universal Life Brokers

Qualified strategies are a much better option than non-qualified plans, they still have concerns not provide with an IUL. Investment options are generally restricted to common funds where your account worth goes through wild volatility from exposure to market danger. There is a huge difference in between a tax-deferred retirement account and an IUL, yet Mr.

You purchase one with pre-tax bucks, reducing this year's tax obligation expense at your marginal tax obligation price (and will certainly commonly be able to withdraw your cash at a lower effective rate later on) while you purchase the other with after-tax bucks and will certainly be forced to pay rate of interest to borrow your very own money if you don't desire to give up the policy.

He tosses in the classic IUL salesman scare technique of "wild volatility." If you dislike volatility, there are far better methods to reduce it than by purchasing an IUL, like diversification, bonds or low-beta stocks. There are no constraints on the amount that might be contributed every year to an IUL.

Why would certainly the federal government placed limits on exactly how much you can put right into retirement accounts? Perhaps, just maybe, it's since they're such a wonderful offer that the government does not want you to save too much on taxes.

{kind=link}

Latest Posts

Universal Aseguranza

Linked Life Insurance

Is Indexed Life Insurance A Good Investment